Exchange-Traded Funds (ETFs) have revolutionized investing for European investors, offering a simple way to build diversified portfolios without the complexity of picking individual stocks. Whether you're just starting your investment journey or looking to optimize your strategy, this guide will walk you through everything you need to know about ETF investing from a European perspective.

We've tested numerous investment approaches, and ETFs consistently emerge as one of the most efficient ways for European investors to build wealth. The combination of low costs, instant diversification, and regulatory protection through UCITS makes them particularly attractive for investors across the EU.

What Is an ETF and How Does It Work?

An ETF is essentially a basket of investments that trades on the stock exchange like a single stock. Think of it as buying a ready-made portfolio in one transaction. When you buy shares of an ETF, you're purchasing a tiny slice of all the investments held within that fund.

ETFs work by tracking an index, sector, commodity, or other assets. The fund manager (or computer algorithm for passive funds) ensures the ETF's holdings match its stated objective. For instance, an S&P 500 ETF will hold the same 500 companies that make up the index, in roughly the same proportions.

The beauty of this structure is that you get professional management and rebalancing automatically. When companies enter or leave an index, the ETF adjusts accordingly without you lifting a finger. The ETF's price fluctuates throughout the trading day based on supply and demand, just like individual stocks.

Benefits of ETFs vs Individual Stocks

We've analyzed both approaches extensively, and ETFs offer several compelling advantages over picking individual stocks, especially for investors who don't have time to research companies thoroughly.

Instant diversification stands out as the primary benefit. Buying one ETF can give you exposure to hundreds or thousands of companies. Achieving similar diversification with individual stocks would require substantial capital and numerous transactions. With ETFs, you're protected from the risk of any single company failing catastrophically.

Cost efficiency makes ETFs particularly attractive. Instead of paying commissions on dozens of individual stock purchases, you make one transaction. The ongoing management fees for passive ETFs typically range from 0.03% to 0.30% annually, which is negligible compared to actively managed funds charging 1-2%.

Time savings cannot be overstated. Researching individual companies, reading quarterly reports, and monitoring news takes considerable effort. ETFs eliminate this burden while still giving you market exposure. Professional rebalancing happens automatically, maintaining your desired allocation without manual intervention.

Tax efficiency in many European countries favors ETFs, though this varies by jurisdiction. The fund structure often allows for more efficient handling of dividends and capital gains compared to frequent trading of individual stocks.

Why UCITS ETFs Are Essential for European Investors

For European investors, choosing UCITS-compliant ETFs isn't just recommended, it's essential for both regulatory and practical reasons. UCITS (Undertakings for Collective Investment in Transferable Securities) provides a standardized regulatory framework across the EU.

UCITS ETFs offer robust investor protection through strict regulatory oversight. Fund assets must be held separately from the fund manager's assets, protecting your investments even if the provider faces financial difficulties. Diversification requirements prevent excessive concentration in single securities, reducing risk.

Tax efficiency improves significantly with UCITS ETFs. These funds can be sold across EU borders without additional regulatory hurdles, and many EU countries offer favorable tax treatment for UCITS funds. Dividend withholding taxes are often reduced or eliminated through tax treaties.

The practical advantages include easier access through European brokers, trading in euros to avoid currency conversion fees, and clear, standardized documentation in multiple European languages. Risk disclosure follows consistent EU standards, making it easier to compare different funds.

Finding and Choosing the Right ETF

Selecting the right ETF requires understanding your investment goals and evaluating several key factors. We recommend starting with JustETF.com, a free database specifically designed for European investors that lists thousands of UCITS ETFs.

Determine Your Investment Strategy

Your ETF selection should align with your investment objectives. Index-based ETFs offer the most straightforward approach, tracking established benchmarks like the S&P 500 or Nasdaq 100. These provide broad market exposure with minimal fees. We covered S&P 500 investing specifically in our detailed guide for European investors.

Thematic ETFs focus on specific sectors or trends like technology, renewable energy, or artificial intelligence. While potentially offering higher returns, they carry concentrated risk and typically charge higher fees. These work best as smaller portfolio allocations rather than core holdings.

All-world ETFs provide maximum diversification by investing globally across developed and emerging markets. Funds like Vanguard's FTSE All-World or iShares' MSCI ACWI give you exposure to thousands of companies worldwide in a single purchase.

Key Selection Criteria

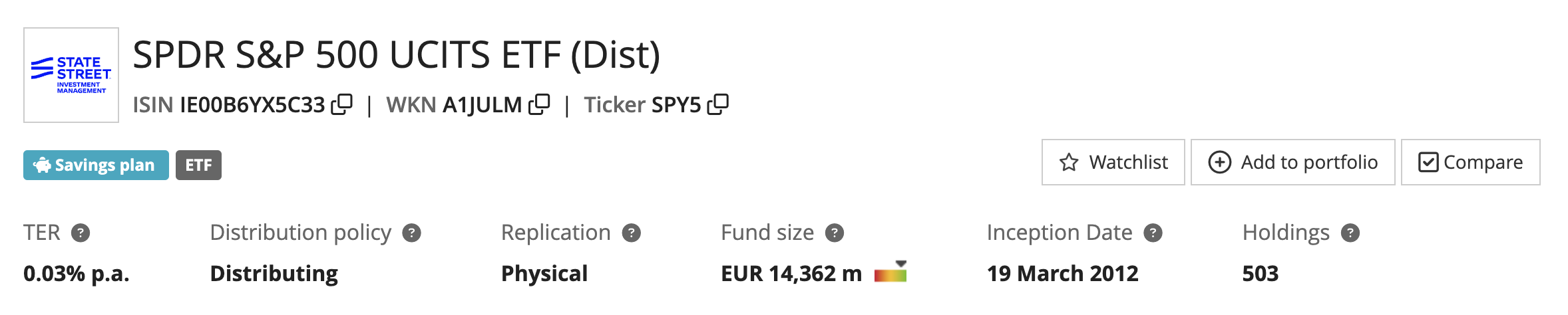

Total Expense Ratio (TER) directly impacts your long-term returns. We've found that even small fee differences compound significantly over time. Aim for TERs below 0.20% for broad market ETFs and below 0.50% for specialized funds. Use our ETF fee calculator to see exactly how fees affect your returns over different time periods.

Accumulating vs Distributing determines how dividends are handled. Accumulating ETFs automatically reinvest dividends back into the fund, perfect for passive, long-term growth without manual intervention. Distributing ETFs pay dividends to your account, providing regular income but requiring manual reinvestment for compound growth. We generally recommend accumulating ETFs for younger investors focused on growth, while distributing ETFs suit those seeking passive income in retirement.

Replication Method affects both risk and tracking accuracy. Physical replication means the ETF actually buys and holds the underlying securities, providing true ownership and minimal counterparty risk. Synthetic replication uses financial derivatives to track performance, which can be more efficient for certain markets but introduces counterparty risk. We strongly recommend physical replication for core portfolio holdings.

Fund Size matters for liquidity and longevity. Larger funds (over €100 million in assets) have better trading spreads and lower risk of closure. The provider's income equals fund size multiplied by expense ratio, so tiny funds may not be profitable enough to continue operating. Avoid ETFs with less than €50 million in assets unless you're willing to accept closure risk.

Track Record and Inception Date provide performance history and reliability indicators. ETFs operating for at least three years have proven their ability to track their index through different market conditions. Newer funds lack this history and may have unexpected tracking errors or operational issues.

Provider Reputation ensures stability and professionalism. The three giants (iShares by BlackRock, Vanguard, and State Street) dominate the market with good reason: rock-solid operations, competitive fees, and extensive UCITS offerings. These providers have the scale and expertise to manage funds efficiently while maintaining low costs.

Setting Up Your ETF Portfolio

Choosing the Right Broker

Your broker choice significantly impacts your investing experience and costs. We've thoroughly reviewed the major European brokers and consistently recommend three platforms for ETF investing.

Interactive Brokers offers the widest ETF selection and sophisticated tools for serious investors.

Lightyear focuses on simplicity and user experience, perfect for beginners. They offer commission-free investing in popular ETFs with an intuitive mobile app that makes regular investing effortless.

Trading 212 provides commission-free ETF investing with fractional shares, allowing you to invest exact euro amounts rather than whole shares.

Automating Your Investments

Automation removes emotion from investing and ensures consistent wealth building. We strongly recommend setting up automatic monthly or weekly investment orders. This dollar-cost averaging approach smooths out market volatility over time.

Most modern brokers offer recurring investment features. Set a fixed euro amount to invest in your chosen ETFs each month, preferably right after your salary arrives. This "pay yourself first" approach prioritizes investing before discretionary spending.

The power of this automated compound growth becomes apparent over time. Our compound growth calculator demonstrates how regular €500 monthly investments can grow to substantial sums over 20-30 years.

Tax Considerations for EU Investors

Tax treatment varies significantly across EU countries, but some general principles apply. UCITS ETFs domiciled in Ireland or Luxembourg often provide the most tax-efficient structure for European investors due to favorable tax treaties.

Accumulating ETFs can defer tax liabilities in many countries since you're not receiving cash dividends. This allows more money to compound within the fund. However, some countries like Germany tax accumulating funds annually on deemed distributions.

Capital gains tax rates and allowances differ by country. Some nations offer generous annual allowances (UK's ISA, France's PEA), while others tax gains progressively. Research your country's specific rules or consult a tax advisor for optimization strategies.

Common ETF Investing Mistakes to Avoid

We've observed investors repeatedly making certain errors that hamper their returns. Over-diversification through owning too many overlapping ETFs adds complexity without benefit. Three to five well-chosen ETFs typically provide sufficient diversification.

Chasing performance by constantly switching to last year's best-performing ETFs guarantees buying high and selling low. Stick with your chosen strategy through market cycles. Similarly, trying to time the market by waiting for the "perfect" entry point often results in missing years of growth.

Ignoring fees might seem minor when TERs appear small, but we've calculated that a 0.50% fee difference can cost tens of thousands of euros over a 30-year investment horizon. Always factor total costs into your selection process.

Neglecting to rebalance when using multiple ETFs can skew your portfolio away from intended allocations. Review and rebalance annually or when allocations drift more than 5% from targets.

Building Your First ETF Portfolio

For beginners, we recommend starting simple with a single all-world ETF providing instant global diversification. As you gain experience and capital, you can add complementary funds for specific exposures.

A basic three-fund portfolio might include:

- 80% All-World ETF (core holding)

- 20% S&P 500 ETF (growth)

Your emergency fund should be fully funded before investing in ETFs. Our 11-point financial health checklist helps ensure you're ready for long-term investing.

Monitoring and Maintaining Your ETF Investments

While ETFs require minimal maintenance, annual reviews ensure your portfolio remains aligned with your goals. Check that your chosen ETFs still track their indices efficiently with low tracking error. We recommend Delta Portfolio Tracker to see your various holdings and brokers in one app.

Review expense ratios annually, as providers occasionally reduce fees to remain competitive. Switching to a cheaper equivalent ETF can boost long-term returns, though consider tax implications before selling.

Monitor fund sizes and provider changes. ETF closures, while rare for large funds, require action to avoid forced liquidation at inopportune times. Most providers give several weeks' notice before closing funds.

Next Steps in Your Investment Journey

ETF investing provides European investors with an efficient path to building long-term wealth. The combination of low costs, instant diversification, and UCITS protection creates an ideal investment vehicle for most portfolios.

Start by opening an account with one of our recommended brokers, selecting your first UCITS ETF based on the criteria we've outlined, and setting up automatic monthly investments. Even starting with €100 per month can lead to significant wealth accumulation over time.

Remember that successful investing is a marathon, not a sprint. Stay disciplined, keep costs low, and let compound growth work its magic over the years.

Frequently Asked Questions

What is the minimum amount needed to start investing in ETFs?

Most European brokers allow ETF investing with as little as €1 through fractional shares. However, we recommend starting with at least €50-100 monthly to make the effort worthwhile.

How many ETFs should I own in my portfolio?

For most investors, 1-3 ETFs provide sufficient diversification without unnecessary complexity. A single all-world ETF can be perfectly adequate for beginners. Adding more ETFs should serve specific purposes like geographic tilts or asset class diversification, not just for the sake of variety.

Are ETFs safe if the provider goes bankrupt?

Yes, UCITS ETFs are extremely safe due to regulatory requirements. The underlying assets are held separately by a custodian bank, not the ETF provider. If a provider like iShares went bankrupt, your ETF shares and their underlying assets remain protected and would be transferred to another provider.

Should I buy distributing or accumulating ETFs?

We generally recommend accumulating ETFs for investors in their wealth-building phase (under 50) as they automatically reinvest dividends for compound growth. Distributing ETFs suit investors seeking regular income or those in countries where accumulating funds face unfavorable tax treatment.

How often should I invest in ETFs?

Monthly investing works well for most people, aligning with salary payments. Some prefer weekly investments for even more averaging, while others invest quarterly. The key is consistency and automation rather than trying to time the market.

Can I lose all my money in an ETF?

While ETF values fluctuate with market conditions, losing everything is virtually impossible with diversified ETFs. Even in severe market crashes, broad market ETFs retain substantial value. The biggest risk is panic selling during downturns, locking in temporary losses.

What's the difference between ETFs and mutual funds?

ETFs trade on exchanges like stocks with real-time pricing, while mutual funds price once daily after market close. ETFs typically have lower fees, better tax efficiency, and no minimum investment requirements. Mutual funds may offer automatic investing directly with the fund company but generally cost more.

Risk Disclaimer: All investments carry risk, including loss of capital. EU Investing Hub does not provide investment advice. Content is for educational purposes only. Always do your own research.