Curve Card promises to consolidate all your payment cards into one smart Mastercard. After extensive testing, we found the concept compelling but the execution seriously lacking. Here's what EU users need to know before signing up.

What We Like About Curve Card

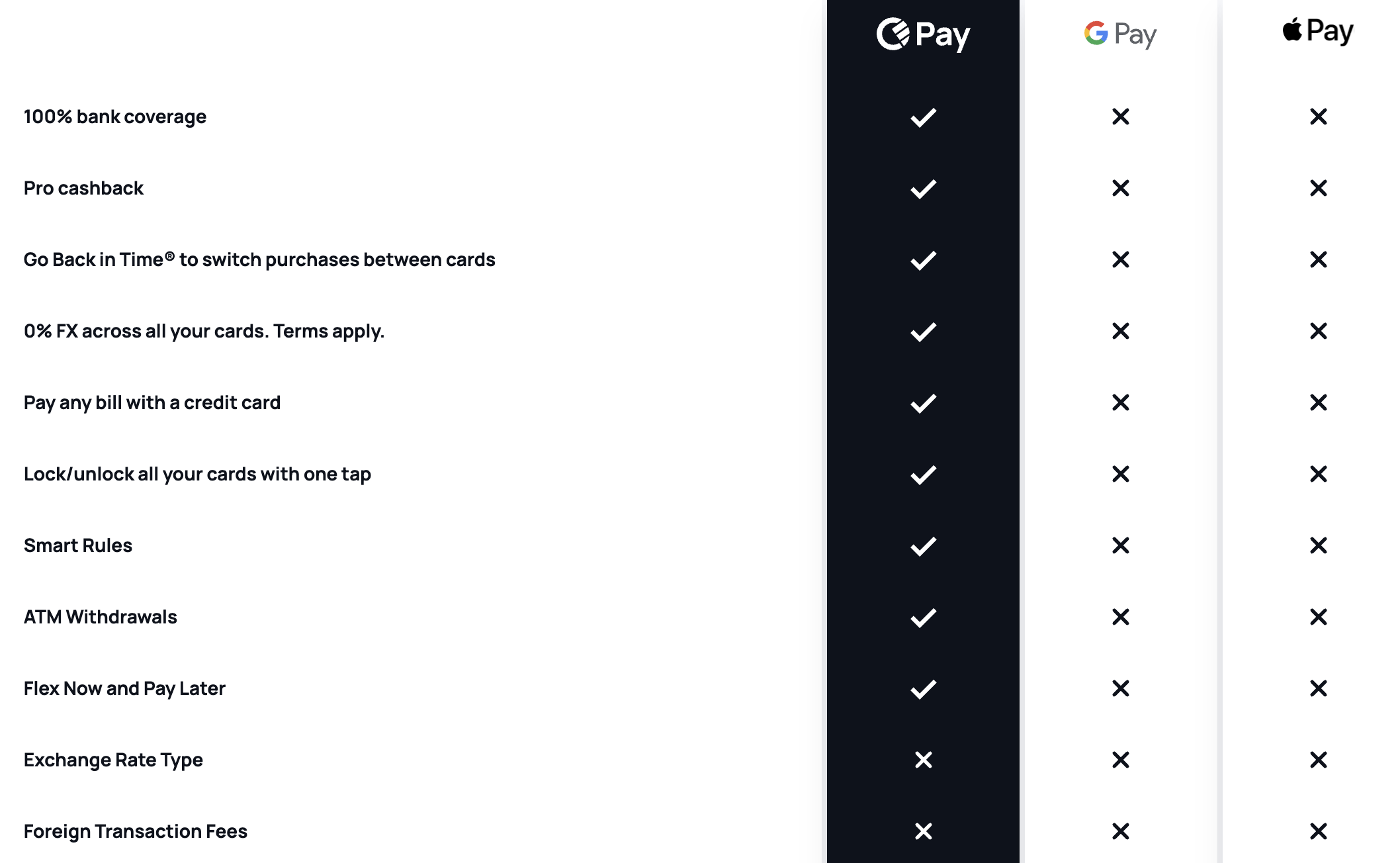

The core concept remains innovative. Curve sits between you and your existing cards, allowing you to:

- Consolidate multiple cards into one physical Mastercard

- Switch transactions retroactively with "Go Back in Time" (up to 120 days)

- Manage spending through one app interface

- Automate card selection with smart rules

The Go Back in Time feature genuinely solves real problems. Moving a personal expense from your business card or switching to a rewards card after purchase works seamlessly when it functions properly.

What We Don't Like About Curve Card

Our testing revealed significant issues that make Curve difficult to recommend:

Severe Free Tier Restrictions: The November 2023 changes gutted the free version. You're now limited to just 2 cards (defeating the aggregation purpose), 3 monthly transaction switches, and €250 foreign spending before hitting 2.99% fees.

Customer Service Crisis: Support response times of 3-4 weeks minimum with no phone support option. Users report cards blocked during travel with no emergency resolution path.

Cashback Problems: Many credit card providers don't offer cashback or rewards when purchases route through Curve, defeating a key reason to use premium cards in the first place.

Curve Card Pricing and Plans

Curve offers four tiers, though we found limited value in most.

The paid plans only make sense if you regularly exceed €250 monthly in foreign spending, but competitors offer better rates without monthly fees.

| Feature | Pay (Free) | Pay X (€5.99/month) | Pay Pro (€9.99/month) | Pay Pro+ (€17.99/month) |

|---|---|---|---|---|

| Monthly Cost | €0 | €71.88/year | €119.88/year | €215.88/year |

| Card Delivery | €5.99 | €3.99 | €0 | €0 |

| Cards Supported | 2 maximum | Unlimited | Unlimited | Unlimited |

| Go Back in Time | 3 per month | 3 per 60 days | Unlimited (90 days) | Unlimited (120 days) |

| FX Allowance | €250/month | €3,333/month | €50,000/month | €100,000/month |

| Excess FX Fee | 2.99% | 2.99% | 2.99% | 2.99% |

| ATM Allowance | €0 (2% fee) | €300/month | €500/month | €1,000/month |

| Cashback | None | None | 1% at 6 retailers | 1% at 12 retailers |

| Our Assessment | Nearly useless | Poor value | Overpriced | Competes with Revolut Metal |

Safety and Regulation

Curve operates under proper EU regulation through Curve Europe UAB in Lithuania (Bank of Lithuania oversight) and Curve OS Ltd in the UK (FCA regulation). Your funds receive standard e-money institution (learn about managing your finances in our 11-point financial checklist) protection.

However, using Curve removes Section 75 credit card protection since your card issuer sees transactions as coming from Curve, not the original merchant. This creates additional risk for expensive purchases.

Trading Experience and App Issues

The Curve app provides decent spending analytics and transaction categorization when it works. However, we encountered:

- Frequent app crashes and login failures

- False positive fraud detection blocking legitimate purchases

- Payment processing errors even with sufficient underlying balances

The onboarding process is straightforward with standard KYC requirements, but card delivery can take 1-2 weeks.

Foreign Exchange Performance

This is where Curve shows both its biggest weakness and potential strength:

Free Tier Problems:

- Severe €250 monthly limit before 2.99% excess fees kick in

- Base rates include Mastercard markup (approximately 0.72% above interbank)

- Essentially unusable for regular travelers due to low limits

Paid Plan Benefits:

- Pay X: €3,333 monthly FX-free allowance

- Pay Pro: €50,000 monthly FX-free allowance

- Pay Pro+: €100,000 monthly FX-free allowance (essentially unlimited for most users)

- No weekend markups (removed in 2022)

- True fee-free spending within limits on paid plans

The Value Question: While paid plans offer genuine FX benefits, you're paying €71.88-€215.88 annually. Competitors like Wise offer mid-market rates with transparent low fees, while Revolut provides competitive rates with much more comprehensive banking features for similar costs.

Customer Support Quality

Customer support represents Curve's most serious failing. We experienced:

- 3-4 week minimum response times for standard queries

- No phone support availability

- Unresponsive email and in-app chat

- Trustpilot rating of just 2.8/5 stars

Users report cards being blocked during travel with no emergency contact options, making any issue potentially catastrophic.

Cashback and Rewards Limitations

A critical issue we discovered: many credit card providers don't offer cashback or rewards when purchases route through Curve. Since card issuers see transactions as merchant category "6051 - Quasi-cash," they often exclude these from rewards programs.

This defeats the primary purpose of using premium rewards cards. If you're not earning cashback on your American Express or Premium Visa, why use them through Curve at all?

How Curve Compares to Alternatives

Versus Revolut: Revolut offers better FX rates, comprehensive banking services, superior customer support and better value for money.

Versus Wise: Wise dominates for international spending with true mid-market rates and transparent fees. No monthly limits or weekend penalties.

Curve's only unique advantage is card aggregation with retroactive switching, but operational issues make this barely usable for free users. Also we recommend having an emergency fund, which should be outside of any of your Curve Cards.

Who Should Consider Curve Card

Curve might work for:

- Business professionals needing expense separation between personal and business cards

- Light international spenders under €250 monthly who can tolerate poor support

Things to Be Aware Of

- Free tier essentially useless after November 2023 changes

- Customer support challenges makes any issue a major problem

- Cashback and rewards often don't work with underlying cards

- Complex fee structure with multiple charges that stack unexpectedly

- No emergency support if card blocked during travel

Final Verdict

Curve Card represents a good idea poorly executed. While card aggregation and Go Back in Time features address real needs, the operational reality falls far short of the marketing promises.

The severe free tier limitations, uncompetitive FX rates, customer service failures, and cashback issues make it difficult to recommend for most EU users. We found alternatives like Revolut, Wise, or modern traditional banks provide better overall value. Also check out the highest yielding savings accounts in Europe.

Curve might improve with their recent €37M funding, but current execution problems make it a risky choice for your primary payment method.

Frequently Asked Questions

Is Curve Card safe to use?

Curve operates under proper EU regulation through Lithuanian and UK authorities. However, poor customer support makes resolving issues extremely difficult if problems arise.

Does Curve Card affect my credit score?

No, Curve is a debit card service that doesn't impact your credit score. However, it may interfere with earning rewards on underlying credit cards due to how transactions are categorized.

Why is the "airport lounge access" misleading?

Curve advertises "airport lounge access" for Pro+ users but actually provides discounted access at €24 per person through LoungeKey, not free lounge entry as the marketing implies.

Can I use Curve Card for cash withdrawals?

Yes, but the free tier has no ATM allowance (2% fee or €2 minimum on all withdrawals). Paid plans offer meaningful allowances: €300 (X), €500 (Pro), €1,000 (Pro+) monthly.

Why don't I earn cashback through Curve?

Many card issuers classify Curve transactions as "quasi-cash" and exclude them from rewards programs, defeating the purpose of using premium cards.

Does Curve offer any sign-up bonuses?

Yes, Curve offers referral bonuses where new users can receive €10 free when signing up through our referral link and completing qualifying transactions. However, given the free tier's severe limitations, consider whether the service meets your long-term needs before signing up.

What happens if my Curve Card is blocked abroad?

This is a major risk. With no phone support and weeks-long response times, a blocked card during travel can become a serious problem with no rapid resolution.

How does Curve make money?

Curve earns interchange fees from merchants plus foreign exchange markups, monthly subscription fees for paid plans, and various transaction charges.

Can I cancel Curve anytime?

Yes, you can cancel anytime through the app. However, getting customer support to resolve any final issues may take weeks.

All investments carry risk, including loss of capital. EU Investing Hub does not provide investment advice. Content is for educational purposes only. Always do your own research.